Trump’s Tariffs Are Harming US Critical Mineral Supply Chains

Jennifer Toy , Sydney Fultz-Waters / Apr 9, 2025Domestic mining operations take almost two decades to start production, write Jennifer Toy and Sydney Fultz-Waters. Here’s what the US should do instead.

A large walking excavator works in a quarry for the extraction of rare metals. Shutterstock

The United States is losing the race toward clean energy. China dominates the global market for manufacturing solar cells, wind turbines, and electric vehicles (EVs) and has invested billions of government funds into the mining and processing of critical minerals since the 70s. Experts predict that China will only continue to dominate thanks to its stable mineral supply chains, lower upfront factory costs, and a strong workforce of scientists and engineers. The current US administration needs to take strategic actions beyond blanket tariffs and long-term mining operations to protect the nation’s critical mineral supply chains.

What exactly are critical mineral supply chains?

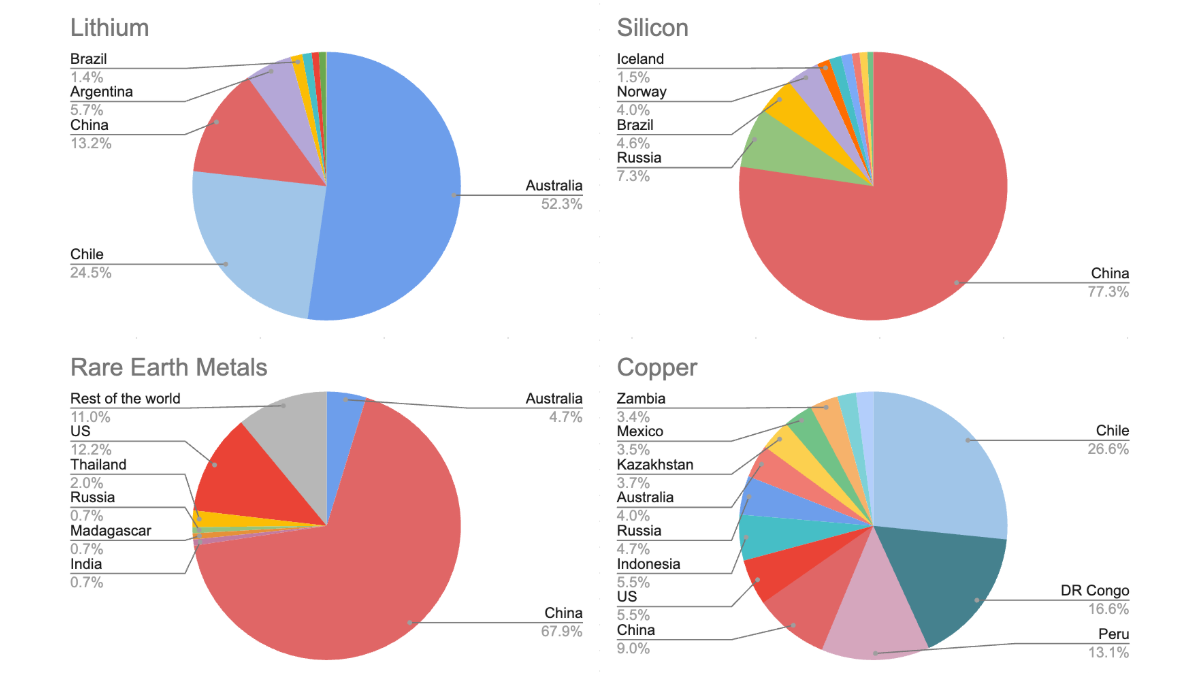

The US Department of Energy defines critical minerals as materials that are at high risk for supply chain disruption and are essential for clean energy technologies. Lithium for batteries, silicon for solar cells, rare earth metals like neodymium for generator magnets in wind turbines, and copper for interconnecting all these technologies are a few examples of critical minerals and their applications. Looking at the breakdown of global production in Figure 1, it becomes clear that the leading nations in mining vary widely from mineral to mineral – and the US is a leading miner of none.

Figure 1: Global production of lithium, silicon, rare earth metals, and copper.

Recent actions taken by the Trump administration to strengthen critical mineral supply chains include substantial tariffs and tariff threats on goods from traditionally allied countries such as Australia, Canada, and Mexico, as well as a new executive order on strengthening domestic mineral production. The tariffs introduced on April 2, 2025, include, but are not limited to, a 35% tariff rate on China, 10% on Brazil, 10% on Argentina, 10% on Peru, and 10% on Australia – just to highlight a handful of the major importers of critical minerals to the US.

Critically, President Donald Trump has also discussed the possibility of a 25% tariff on copper imports to match existing tariffs on steel and aluminum and is currently discussing increasing the tariff rate on China to 50% to discourage the reciprocal tariffs that China has leveraged against the United States. (Editor's note: On Tuesday, April 8, the White House announced an increase in levies on Chinese goods to 104%. That rate took effect just before publication.)

How do Trump’s current tariffs fit into previous efforts to strengthen the domestic supply chain?

This is not the first time that tariffs have directly impacted clean energy technologies. Critical mineral supply chains for clean energy have been a concern since the Obama administration. Even during his first term, Trump focused his efforts on streamlining mining permit processes and encouraging automakers to move their electric vehicle production facilities to the US through trade agreements with Mexico and Canada (the United States-Mexico-Canada Agreement, USMCA).

More recently, the Biden administration levied several tariffs on critical mineral products for EVs and clean energy technologies such as batteries and solar cells. This included a 25% tariff rate on EV batteries, a 50% tariff rate on semiconductors, a 100% tariff rate on electric vehicles, and a 50% tariff rate on solar cells, along with a 25% tariff on graphite and permanent magnets to be implemented in 2026. However, as part of his “carrot and stick” approach, President Joe Biden also provided subsidies for consumers on domestically manufactured EVs and heavily invested in clean energy technologies. This approach included “friend-shoring” and on-shoring mining and processing to reduce reliance on China for critical minerals without jeopardizing relations with US allies.

With the second Trump administration came new foreign trade policies, including blanket tariffs on several key mineral importers to the US, including China, Australia, and Brazil. In retaliation, targeted nations have levied reciprocal tariffs on the US, and China has gone as far as placing export controls on five critical minerals: tungsten, tellurium, bismuth, indium, and molybdenum, to the US active February 4, 2025. It is important to note here that in addition to tariffs, the Trump administration is working on accelerating mining operation permits and loan processes to improve domestic mineral production. These efforts will likely shorten the time required to bring a mine to production in the long term and play an important role in strengthening the domestic supply chain. However, it may not be fast enough to meet the current demands of clean energy technologies.

Why do blanket tariffs not work for clean energy technologies?

A key issue with the current tariffs is their lack of strategic pressure. Take the case of electric vehicles as an example. Tariffs on raw minerals from countries like China have little impact on the price of the critical minerals for an EV, even though an EV includes many more times the amount of critical minerals than a conventional car.

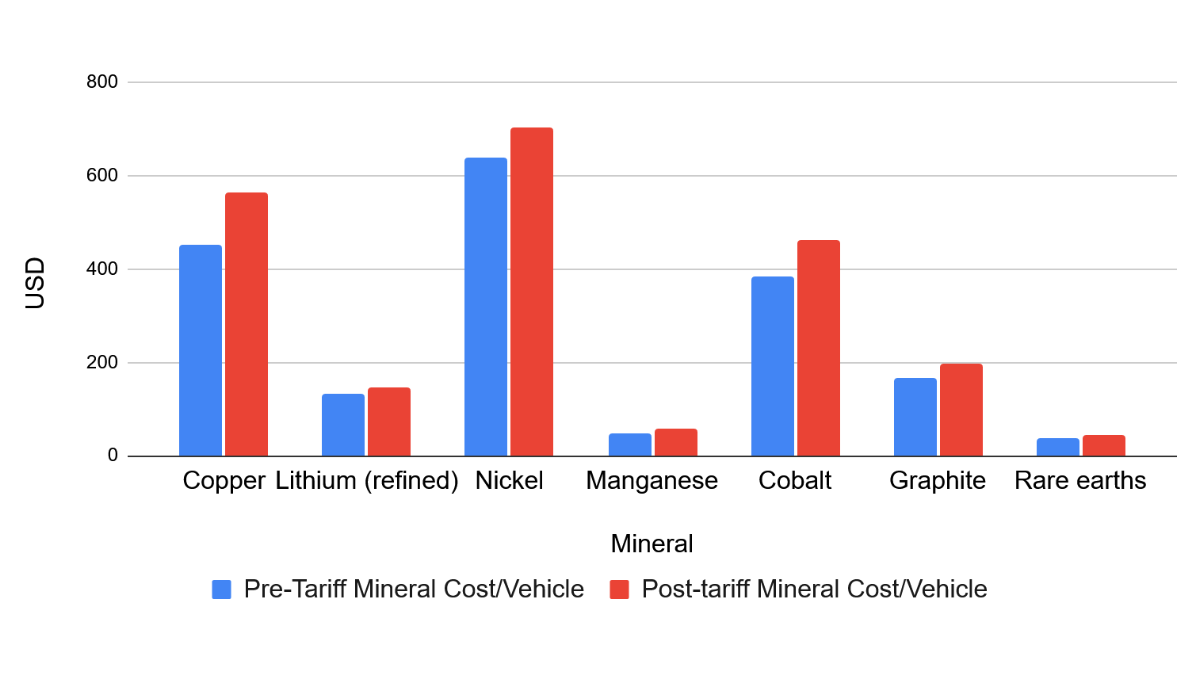

Let’s look at a quick calculation of the impact of tariffs on raw critical minerals (Figure 2). When taking into account the various tariffs levied on Canadian critical minerals (10%), the proposed tariff on copper (25%), and the increased tariff on Chinese critical minerals (possibly up to 50% as of April 7th), the overall increase in mineral cost/vehicle comes out to about 27%, resulting in a $500 increase in the total cost of the car.

These calculations indicate that the overall cost increase from minerals is relatively low compared to the cost of the final product. Since automotive manufacturers often have small profit margins and the tariff landscape is changing daily, manufacturers will likely choose to pass these costs along to consumers rather than make the substantive effort to seek alternative mineral or car part suppliers. The temporary nature of tariffs, especially in a volatile administration, and the lack of tax credit incentives for domestic mining leave hardly any incentive for US companies to invest in a long-term, capital-intensive industry like mining.

When used strategically, tariffs can be beneficial for strengthening supply chains. By incentivizing domestic production and reducing reliance on foreign entities, especially our global rivals, it is possible to protect against supply disruptions like the chip shortage during the COVID-19 pandemic and currently with the national egg shortage. Perhaps one day, we can build a domestic supply of critical minerals strong enough to have a critical reserve similar to the Strategic Petroleum Reserve to limit market volatility. But to reach this point, economic policies must be strategic and carefully designed.

It is unlikely that these current tariffs will be successful in shifting supply chains for critical minerals to US soil. Instead, these policies broadly impose costs on EVs and many other technologies without actually creating market incentives for manufacturers and suppliers to invest in domestic supply chains. There are a few reasons for this:

- Critical mineral supply chains cannot be created by levying a blanket tariff. Blanket tariffs fail to account for the variations in global supply and demand between minerals. Retaliatory tariffs instated by targeted nations will only impose economic strain on both parties.

- Tariffs are too transient to provide domestic producers enough incentive to start businesses. The fact that a tariff can be retracted as quickly as it is raised leaves domestic producers and investors unsure about how long they will receive price premiums, often leading to increased volatility in the market. According to Dr. Karan Buhwalka of Stanford University’s Precourt Institute for Energy, “it’s a matter of there being so much uncertainty about whether it’ll last that [most companies] will not have really committed to really long term contracts.”

- Many businesses choose to continue buying from the same international producers even with the cost hike, and any additional cost trickles down to the consumer.

Make no mistake, this is a complex issue. As Dr. Buhwalka puts it, “There is a tension between whether your priority is scaling up renewable energy technology at a low cost versus domestic security.” This leads administrations to take differing approaches that sometimes contradict each other and ultimately make little to no forward progress in strengthening US critical mineral supply chains. Each incoming administration has the chance to set the stage for smart, long-lasting policies to generate impactful change.

So what can be done?

Though the US lags decades behind in mineral production for clean energy, there are many steps the government can take to put us on the right track. Here are a few that the current administration could take:

- Removing blanket tariffs: Angering allied partners is not helping the US form stronger supply chains toward protected mining and processing supply chains. The US cannot be its sole producer and developer of clean energy technologies that rely on critical minerals, so we must invest in partnerships across the globe.

- Keep long-term government investments in critical minerals and clean energy: Domestic mines take, on average, 16 years to begin production. In the meantime, consumers and companies need incentives to continue investing in clean energy through subsidies like those during the Biden administration.

- Implement price volatility management: To compete with China’s artificially cheap mineral costs and the volatile nature of the mineral market, we should use tools like floor pricing or contracts-for-difference to protect domestic producers.

- Focus future government investments in mineral processing and recycling: While the US has significant domestic mineral supplies and investments into mining operations and is currently increasing efforts into mining operations, there is a significant lack of refining and processing plants to transform the raw material into refined minerals to be used in final products. Dr. Buhwalka describes it as “focusing tariffs on the products that you’re very confident will scale domestically.”

The global transition to clean energy is well underway and will continue to accelerate. The question remains: Will the US be prepared to participate as a leader in this transition, or will it be left behind? Today's policies will not only determine the future of US energy and security but also its influence on the global energy stage for generations to come.

Authors